We started 2022 with hopeful and patriotic hearts as many turned their eyes and television sets towards the Beijing Winter Olympics to watch their favorite snow sport. These particular Games seemed aptly timed to coincide with the Chinese Zodiac, which entered the Year of the Tiger. Just like the catchy song goes, the tiger symbolizes bravery, competitiveness and confidence; something every athlete aims to be. While the games played out, there was the usual bit of drama; emotional breakdowns on the ski slopes and drug doping issues on the ice rink. However, the real drama was unfolding on the periphery--the boarder of Ukraine. While competitors strapped on skis and skates and curlers grabbed their brooms, Russia was putting someone else on ice.

Instead of a Bengal tiger, this year came in the form of a cat with different stripes--a Siberian tiger waging war from the North. While tigers have many attractive traits, they are also known to be unpredictable, impetuous, and irritable. They have stubborn personalities, tough judgment, express themselves boldly, and act in a high-handed manner. They are authoritative and never go back on what they have said. Is this sounding like someone we know?

While this war is different, it is still a Cold one! On top of COVID disruptions, we now see how fragile our supply chain issues really are, with Europe experiencing the brunt due to their dependency on Russian energy (Europe gets more than 40% of its natural gas and nearly 30% of its crude oil from Russia). This is leading to a de-globalization of the global economy as countries realize they cannot depend on former trading routes and partners and must secure new solutions. It is also exacerbating what were already high food and energy costs. With Ukraine being a major wheat producer, the Christian prayer asking to “give us our daily bread”, is becoming all too real.

Back on Terra Firma (U.S. soil), the Fed has officially removed the word “transitory” from its language and raised rates (Fed Funds) by 25 basis points to begin combatting inflation. Inflation hit a 40-year high in February, rising 7.9% year-over-year (less food and energy: +6.4%). Energy rose nearly 26% YOY, food prices were up 8%, and gains were also seen in new and used vehicles, shelter, and restaurants/hotels. Meanwhile, the labor market remains strong, with unemployment falling to 3.6%, which is only feeding the beast as higher wages become more sticky.

While we are all experiencing “pain at the pump”, (the average U.S. regular retail gasoline price for the first three weeks of March 2022 was $4.22/gal.) the U.S. is in a much different place than it was back in the 70’s and even as recently as 2008. Thanks to the explosion of shale oil production, the U.S. is no longer a net importer of oil. While higher oil prices make the consumer feel poorer in the short run, the domestic energy producer is richer, and that money keeps circulating in the economy helping to offset some of the gasoline grief. The consumer is also in a much better economic situation now due to the reopening of various parts of the service sector, higher savings relative to history, lower debt levels, and higher accumulated net worth from stock market and housing gains (Case-Shiller Home Index rose 19.2% YOY in January), giving them confidence that they should be able to weather the storm.

Uncertainty creates volatility, and markets have reacted, with some indices entering correction territory. A rebalance between high flying growth stocks and stalwart blue chips has been in motion and continues to play out as interest rates rise, sending bond prices in the opposite direction. While a combination of monetary and fiscal tightening could eventually lead us into a recession, we do not foresee a dead-cat bounce. We do believe exposure to hard assets and non- traditional income generating investments will serve as good diversifiers in this environment.

Closing Thoughts

Although the start to this year has been less than ideal, the silver lining is that the Tiger is also known to be “exorcising”, with the ability to drive out evil from a person or place. While Ukraine’s coat of arms hosts a lion instead of a tiger, let’s hope this cat has what it takes to reclaim the jungle. Another bright spot resulting from this conflict is that just as the globe seemed to be pulling apart, a uniting front is pulling us back together as countries around the world collectively impose sanctions on Russia and denounce its actions. The bad news is that even if the war ends tomorrow, sanctions will stay in place for some time, potentially extending supply chain issues, further aggravating inflation and slowing growth. At least there is some comfort in knowing that we are all in this together! It is in times like these that we emphasize that slow and steady (and honorable) wins the race, and sticking to a disciplined investment process and well- defined long-term asset allocation policy is key to navigating volatile markets and personalities.

Regards,

John P. Ulrich, CFP®

President

Whitney E. Solcher, CFA®

Chief Investment Officer

Equity Markets

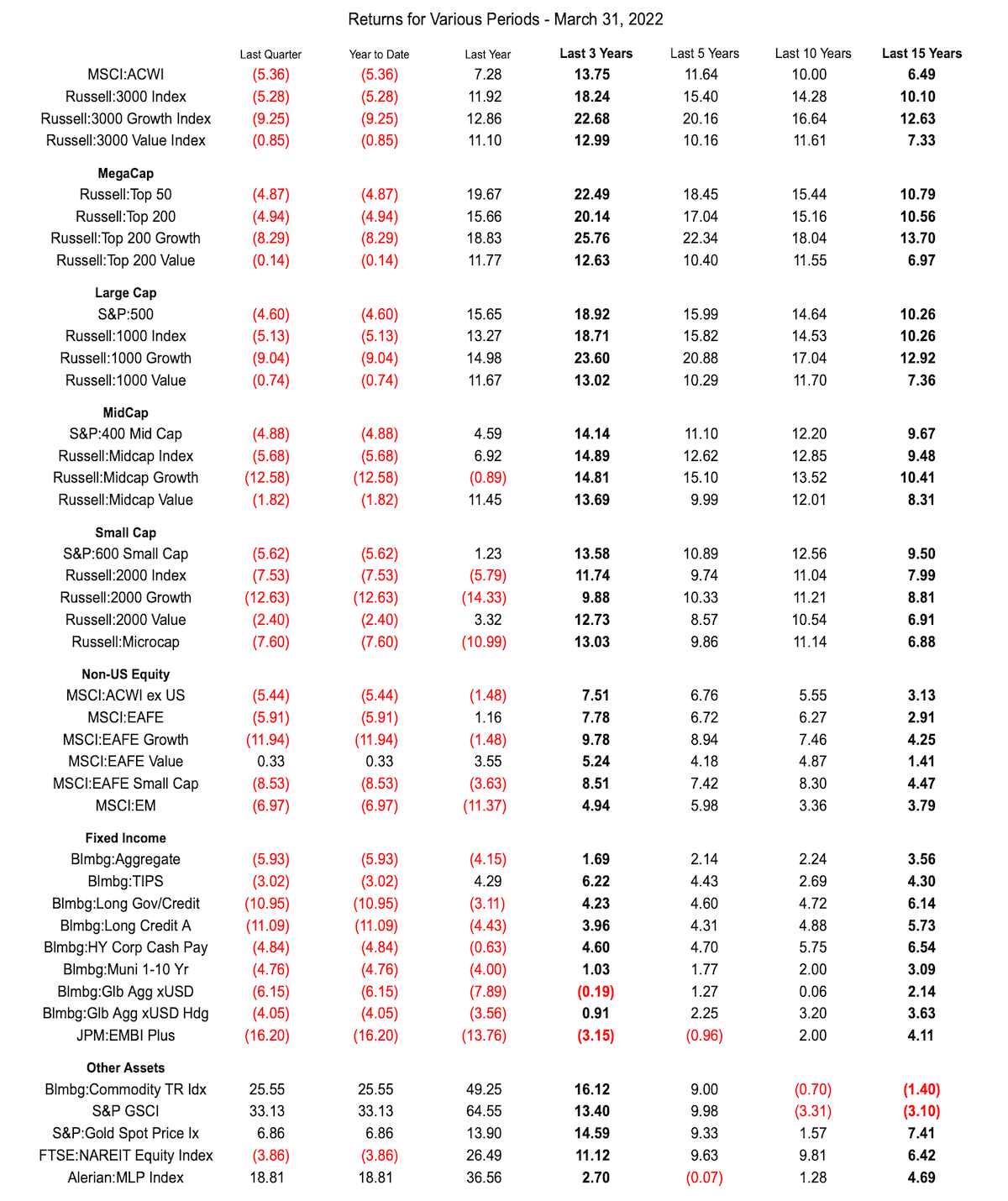

The S&P 500 Index was up a modest 0.6% in 3Q with results mixed across sectors. Industrials (-4.2%) and Materials (-3.5%) were at the bottom of the pack while Financials (+2.7%) were the best performers. Since the market low in February 2020, the S&P is up 97.3%. Growth stocks outperformed value (R1000 Growth: +1.2%; R1000 Value: -0.8%) but lag for the YTD period (+14.3% vs. +16.1%). Small cap stocks underperformed (R2000: -4.4% vs. R1000: +0.2%) and now lag YTD (12.4% vs. 15.2%).

The MSCI ACWI ex-USA Index lost 3.0% for the quarter, hurt primarily by U.S. dollar strength and the benchmark's exposure to emerging markets. The best-performing sector was Energy (+7%), while Consumer Discretionary (-11%) and Communication Services (-10%) posted steep declines. Note that these sectors include some of the Chinese stocks that have been hit hard by the country's regulatory crackdown (Alibaba, Tencent, and Baidu). The MSCI EAFE Index (Europe, Australia, and Far East) lost 0.4% but in local terms it was up 1.3%. Japan (+4.6%) performed relatively well while many of the larger constituents were down for the quarter. The MSCI Emerging Markets Index sank 8.1%, making it the worst-performing asset class for the quarter. Within emerging markets, Brazil (-20%), China (-18%), and Korea (-13%) fell sharply while India (+13%), Russia (+10%), and Colombia (+10%) were up strongly.

Fixed Income Markets

Yields in the U.S. were relatively unchanged from 6/30/21, masking intra-quarter volatility. The 10-year U.S. Treasury closed the quarter at 1.52%, up sharply from early August when it traded at 1.19%. TIPS outperformed nominal Treasuries for the quarter (Bloomberg US TIPS Index: +1.8%; Bloomberg US Treasury Index: +0.1%). The Bloomberg US Aggregate Bond Index returned 0.1% but remains down 1.6% YTD. Lower quality continued to outperform. The Bloomberg High Yield Index rose 0.9% and leveraged loans (S&P LSTA Lev Loan: +1.1%) also performed well. Municipals (Bloomberg Municipal Bond Index: -0.3%) underperformed Treasuries for the quarter.

Overseas developed market returns were similarly muted, and U.S. dollar strength eroded returns for unhedged U.S. investors. The Bloomberg Global Aggregate ex-US Bond Index fell 1.6% but was flat (+0.1%) on a hedged basis. Emerging market debt posted negative returns; the JPM EMBI Global Diversified Index fell 0.7% and the local JPM GBI-EM Global Diversified Index lost 3.1%, most of which was due to currency depreciation. In local terms, this Index was down only 0.2% for the quarter.

Real Assets

The Bloomberg Commodity Index rose 6.6% for the quarter and is up 29.1% YTD, but what lies under the hood is more interesting. Natural gas prices soared nearly 60% for the quarter, and those gains were relatively muted compared to the experience in Europe, where prices tripled over the quarter. WTI Crude Oil was up 4%. TIPS (Bloomberg TIPS Index: +1.8%) performed well relative to nominal U.S. Treasuries. Several other sectors were essentially flat for the quarter; the MSCI US REIT Index gained 1.0%; gold (S&P Gold Spot Price Index: -0.8%) and infrastructure (DJB Global Infrastructure: -0.9%) fell slightly. Copper fell more than 4% on worries over slowing demand from China.

The views expressed represent the opinion of Ulrich Investment Consultants. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from sources that have not been independently verified for accuracy or completeness. While Ulrich Investment Consultants believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward- looking statements are based on available information and Ulrich Investment Consultants’ view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.