I recently had the great fortune of taking a vacation to Europe, our first major excursion in nearly seven years. It was a wonderful change of scenery, culture and most importantly, climate! The summer heat had not quite hit the Mediterranean, and it seemed that the moderate temperature coincided with the sanguine attitude of the Croatian people. We toured towns and castles along the Adriatic that had been fought over since the 4th century BC. While traversing the beautiful coastline, engaging with the locals, eating fabulous seafood (and sampling sumptuous wine), it became obvious why this small country has traded hands so many times throughout the centuries; it is clearly worth fighting for. The Croatians know it too and are an extremely proud and patriotic people. Their red, white, and blue flag flies high throughout the country and the seaside.

It was a refreshing contrast to what feels like a more tepid enthusiasm from the American public, even on the dawn of our nation’s birthday. In fact, last year’s Gallup poll marked the lowest rating on record, at 38% of people who said they were “extremely proud to be American.” Believe me, there’s plenty of people at the border that will take the other 62%! So, what gives? Perhaps it is rising interest rates, inflation, Covid overhang, or our divided political system, but the whole world is experiencing the same thing. While overseas, I did not hear one complaint about these current issues; people were just happy to be out and about -- to be living life. And maybe therein lies the real problem. Americans watch too much tv, work too hard, and simply “live” less...at least that’s what the Europeans think!

At home, we continued to watch the Fed hike rates yet another 25 basis points to 5.25%, despite steadily falling inflation data (CPI fell to 4.0% in May vs. 8.6% the year before). Manufacturing continues to be in decline, with PMI data showing seven consecutive months of contraction. Credit continues to tighten in the wake of the regional banking crisis, just as excess consumer savings is running off. This should continue to worsen, with the expiration of the pause in student loan interest, which has been in place since March 2020 (Americans owe roughly $1.8 Trillin in student debt). In “good news”, unemployment actually rose to 3.7%, although the Fed still huffed that they were “overachieving” their goal of maximum employment, sending stock markets railing after what had been a fairly strong quarter (the S&P is up roughly 8.7%). The much-anticipated debt ceiling debate was all bark and no bite, with neither side really winning or losing. New home sales surged despite mortgage rates at 7%, and consumer confidence appears to have brightened a bit.

Meanwhile overseas, the news was a bit louder, as there was a twist in the ongoing Russian/Ukraine conflict. Putin was forced to take a double take when his former close, confidant and leader of the Wagner Group, Yevgeny Prigozhin, launched a coup d’etat on the Russian army. Wagner is a Russian state-backed mercenary group that was supporting the Russian army and leading most of its successes. Due to lack of military leadership and direction, Prigozhin publicly decried Russian government justifications for the invasion of Ukraine and accused the Russian Defense Ministry of “trying to deceive society and the president and tell us how there was crazy aggression from Ukraine and that they were planning to attack us with the whole of NATO”. He then switched team jerseys and staged a mutiny, marching his troops towards Moscow, exposing Putin’s vulnerabilities and creating the biggest threat to his position of power in 23 years. Prigozhin proceeded to shoot down a military plane and several helicopters (“Kaboom”) and seized a major Russian military hub, while Russian military troops seemingly “stepped aside”. Some soldiers even welcomed him with their own red, white, and blue flags and began requesting selfies with the rogue leader. This short-lived mutiny came to a halt roughly 100 miles outside of Moscow when President Lukashenko of Belarus managed to negotiate a deal that allowed Prigozhin and a few other military leaders to retreat gracefully to his country, leaving Putin to fight another day. Putin may be licking his wounds; however, a caged animal can be more dangerous than a healthy one, so let’s hope this Siberian Tiger doesn’t push the red button.

Finally, let’s not forget about the ongoing antics of the fiery, “Little Kim” Jong Un who has been ramping up tensions in the Korean Peninsula and test-firing short-range weapons. The US responded by sending its largest, nuclear-armed submarine to South Korea (an ally, also bearing the red, white, and blue) for the first time in four decades. Together, the US and South Korea have been conducting joint exercises further fueling China’s fury..

Closing Thoughts

On the backside of our European excursion we decided to exit via France; yet another country that shares our banner’s color scheme. We hit Paris, the home of haute couture, on the eve of Fashion week. This city sets the stage for what will define “the look” for the coming season and based on my limited window shopping I can tell you this year’s color palette is no other than red, white, and blue. Not surprising since Paris will be hosting the 2024 Olympic Games and felt the need to feed a little patriotism into their country’s wardrobe. Who can blame them?

Just like flags, our clients come in all shapes and colors. They have different needs and goals, but at the end of the day they are all human. In times of uncertainty and volatility, being human can sometimes be the hardest job of all. At Ulrich, we are here to guide you and hoist and lower your flag to adjust and adapt to the changing winds of time.

In closing, we wish everyone a Happy 4th of July, and lest we forget, while many countries may share our sovereign colors, we’ll take the freedom of our stars and stripes over any other pattern!

Regards,

John P. Ulrich, CFP®

President

Whitney E. Solcher, CFA®

Chief Investment Officer

Equity Markets

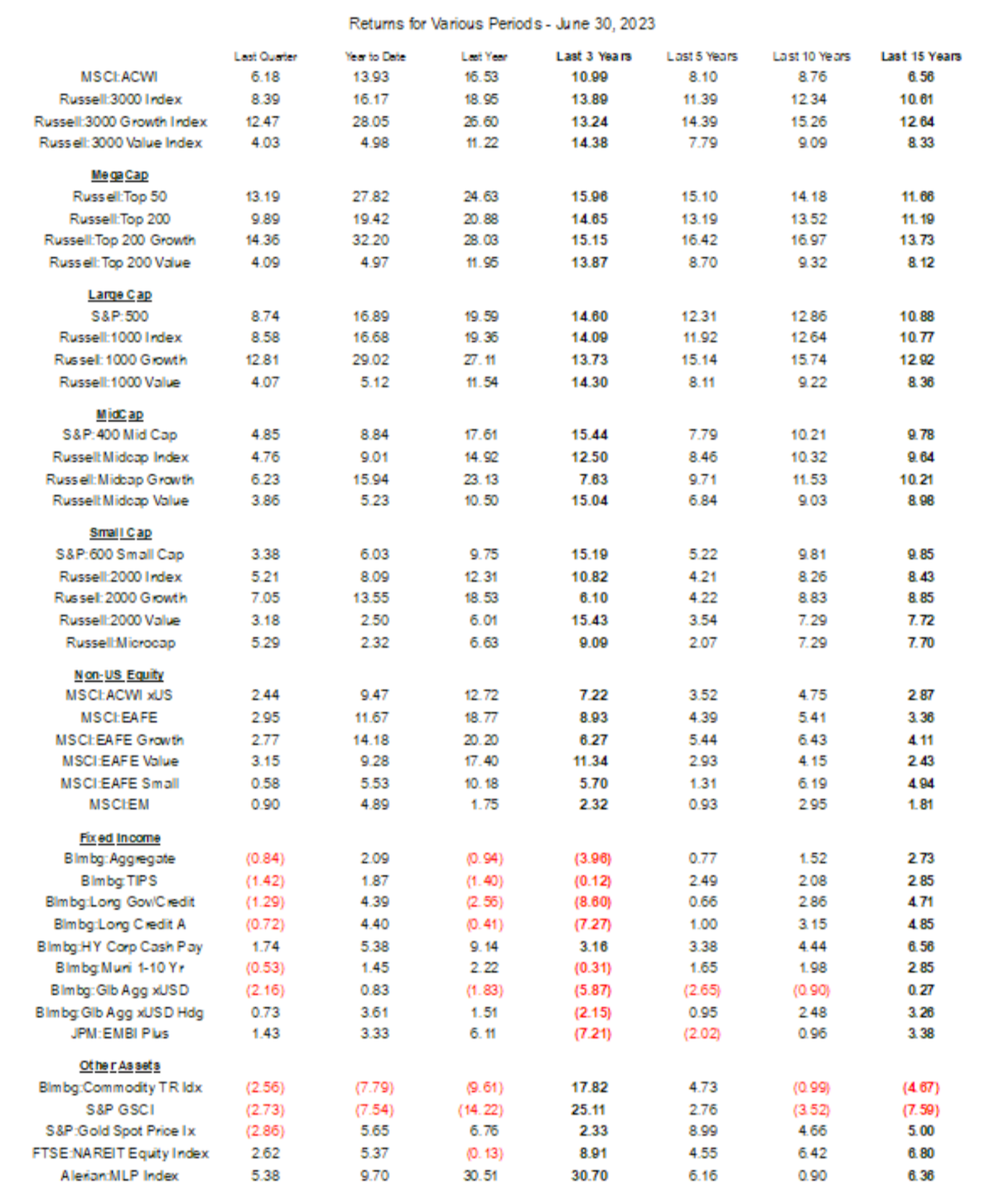

U.S. stock indices posted positive returns in 2Q with performance dominated by large cap stocks. The S&P 500 Index rose 8.7% (+16.9% YTD) while the tech-heavy Nasdaq Composite returned +13.1% (+32.3% YTD), its best six-month performance since 1999. The 2Q top contributors, coined the “Magnificent Seven,” were Nvidia (+52%), Meta Platforms (+35%), Amazon (+26%), Tesla (+26%), Apple (+18%), Microsoft (+18%), and Alphabet (+15%). The Index is now the most concentrated that it has been since the 1970s with those stocks accounting for about 25% of the market cap of the Index (and nearly 50% of the Nasdaq). (Of note, the equal-weighted S&P 500 Index was up 4.0% in 2Q and 7.0% YTD). Within the S&P 500, Technology (+17.2%), Communication Services (+13.1%), and Consumer Discretionary (+14.6%) rose sharply while Energy (-0.9%) and Utilities (-2.5%) fell. Growth stocks trounced value for the quarter (Russell 1000 Growth: +12.8%; Russell 1000 Value: +4.1%) due largely to the sharp outperformance of Technology relative to Health Care, Energy, and Financials. Small cap stocks underperformed large (Russell 2000: +5.2%; Russell 1000: +8.6%) across the style spectrum.

Global ex-U.S. equity markets (MSCI ACWI ex USA: +2.4%) trailed U.S. equity markets in 2Q given lower technology exposure. Lacking the U.S. market’s exuberance for any company associated with AI, style impacts in developed ex-U.S. equity were more muted with value (MSCI World ex USA Value: +3.1%) in line with growth (MSCI World ex USA Growth: +3.0%). Illustratively, Industrials (EAFE Industrials: +6.4%) outperformed Technology (EAFE Technology: +5.9%). Japan (+6.4%) was a top performer and its Nikkei 225 Index hit its highest level since 1990. The U.S. dollar appreciated versus the Japanese yen (-7.9%) but fell versus the British pound (+2.8%) and was relatively flat (+0.4%) versus the euro.

Emerging market equity (MSCI EM Index: +0.9%) underperformed developed market equity but results varied widely. Emerging Europe (+11.2%) and Latin America (+14.0%) posted double-digit results while Emerging Asia (-0.8%) was hurt by poor performance from China (-9.7%), Malaysia (-8.4%), and Thailand (-8.2%). The economic news out of China remains muted and uncertain.

Fixed Income Markets

The Bloomberg US Aggregate Bond Index fell 0.8% in 2Q as interest rates rose. A “risk-on” environment bolstered returns for credit and securitized sectors, both of which outperformed U.S. Treasuries on a duration-adjusted basis. The lowest- quality bucket of the Index (rated BBB) also performed best. The 10-year U.S. Treasury yield was 3.81% as of quarter-end, up from 3.48% as of 3/31. The yield curve was sharply inverted at quarter-end with the 2-year U.S Treasury yielding 4.87%. High yield (Bloomberg High Yield Index: +1.8%) performed well amid robust risk appetite, muted issuance, and promising economic news. Munis outperformed U.S. Treasuries: the Bloomberg Municipal Bond Index dropped 0.1% and the shorter duration 1-10 Year Blend was down 0.5%. As with taxable bonds, lower quality outperformed (Bloomberg Municipal Bond BBB: +0.7%; Bloomberg Municipal Bond AAA: -0.4%).

The Bloomberg Global Aggregate ex USD Index fell 2.2% (hedged: +0.7%). Currency played a strong role in results across countries this quarter with mixed performance from the U.S. dollar. Japan (-8.0%) was the worst-performing constituent, due largely to yen deprecation. Emerging market debt indices performed well (JPM EMBI Global Diversified: +2.2%; local currency JPM GBI-EM Global Diversified: +2.5%). Returns were mixed in the local currency index; Latin America (+11%) performed well with double-digit returns from Brazil (+12%) and Colombia (+23%) while Asia (-2%) was hurt by China (- 4%) and Malaysia (-4%). Turkey (-29%) also posted a sharp decline.

Real Assets

The S&P GSCI sank 2.7% in 2Q. WTI Crude ended the quarter at $70.64/barrel, down from $75.67/barrel on 3/31. Copper (-8%) fell on concerns over ebbing global demand and a slowdown in China, and gold (S&P Gold Spot Price: -2.9%) was hurt by lowered expectations for inflation reduced safe-haven demand. REITs were a bright spot (MSCI US REIT: +2.7%) while TIPS (Bloomberg TIPS: -1.4%) were hurt by rising interest rates.

The views expressed represent the opinion of Ulrich Investment Consultants. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from sources that have not been independently verified for accuracy or completeness. While Ulrich Investment Consultants believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Ulrich Investment Consultants’ view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.