We trust the 4th of July holiday left you with a sense of pride and a patriotic feeling in your heart, if not the feeling of heartburn from indulging in the obligatory hot dogs and hamburgers that help define this great backyard grilling nation. As we leave America’s birthday in the proverbial smoke, we turn towards another celebration that only happens every four years. No, not the Presidential election (I did say a “celebration” didn’t I) but the 2024 Summer Olympic Games! Yes, it’s time to don your red, white and blue as athletes from around the globe descend upon the streets of Paris for sixteen days of glory. This festival showcasing athletic excellence will be a welcome reprieve from the “everyday” monotonous, and sometimes depressing news. The Games will be a time to escape the deluge of headlines related to heat waves, floods, gang violence, failing infrastructure, campus protests, details of Elon Musk’s latest pay package, and of course…Taylor Swift’s whereabouts.

Given the unsettled world we have been living in, we hope this culmination of countries and cultures will bring people together in more ways than just sports. Geopolitical tensions of late have been intense, with a never-ending war in Ukraine, unresolved chaos and conflict in the Middle East, cybersecurity terrorist attacks from China, and Russian submarines stationed off the coast of Cuba, just to name a few. Perhaps for a few days we can trade tanks and missiles for stopwatches and javelins and an axis of evil for gold, silver and bronze medals.

After a brief respite, we can then redirect our attention to the other four-year battle at hand with the upcoming run for the White House that is sure to be its own fireworks show. Some may argue that the recent debate was anything but explosive as I do not believe the words “disaster” (Source: CNN, Fox News, The Atlanta Journal) and “train wreck” (Source: The Independent) have ever been used when describing a presidential debate. Even more unlikely, this performance actually appeared to unite the otherwise polarized television networks and many individual voters as well. In case you missed it, and no matter which stripes you wear, it is commonly acknowledged that POTUS was missing a step or two during debate night, and when a fight broke out between the former and current leaders about their golf handicaps…well, let’s just say Saturday Night Live will have a lot of content to work with.

Sparing the pyrotechnics, the outcome of the debate does have some potentially incendiary consequences and puts into question whether a new candidate will arise out of the ashes at the upcoming Democratic National Convention in August. Nothing like taking it down to the wire! Subsequent to the debate, odds on Biden’s presidential victory rose from 5-6 to 4-1 in Las Vegas overnight (higher odds implying a less likely win) while Trump’s fell to 8-15. The clock is ticking, and time will tell which victor gets the spoils, in an election with the highest disapproval rating of both candidates in the history of the poll. Finally, it would seem Americans have something that they can all agree upon.

It is somewhat daunting to draw a comparison between this race and to the many contests that will be hard fought in Paris. Many of these athletes have spent their whole lives preparing for this moment. Imagine the years of practice, sacrifice and self-discipline they have endured, all designed to condition their bodies and minds to qualify for the opportunity to be the best in the world. Alternatively, what do we require from our politicians? What qualifications do we demand in order to serve the American public and lead our great country? The constitution only lists three: the President must be at least 35 years of age, be a natural born citizen, and have lived in the United States for at least 14 years. As far as representing the Stars and Stripes goes, the best of the best may be out on the field instead of in the Oval Office.

As we await the outcome in November, there is another score that people are watching; Fed Funds. While Jay Powell has been extremely patient, we are starting to see signs of lower inflation and growth. The PCE inflation data showed no increase in May and year-over-year came in at 2.6%, below the previous reading of 2.7%. ISM manufacturing came in at 48.5% for June, below the forecast of 49.2% (any reading below 50 signifies contraction). First quarter GDP was revised downward to 1.4% from 1.6%. Unemployment remains stable at 4%, however, there has been an increase in labor participation. Consumer spending, especially at the lower end, has been softer than predicted and credit card and auto loan delinquencies are on the rise. All of this is pointing towards a potential rate cut in September, where the probability has moved to 73.6% as of July 5th from 46.6% a month ago. In this case, bad news may be good news as lower rates should help small business, which is the driver of the American economy.

Closing Thoughts

No matter your game of choice, whether it be swimming, diving, track and field or gymnastics, there will be plenty of sports eye-candy over the coming weeks for everyone to enjoy. Even break-dancing (or “breaking” as it is now known) is making its Olympic debut; the only “game” that requires its own DJ. As an avid equestrian, I will personally be watching the equine activities, which is unique in that it is the only Olympic sport where men and women compete on equal terms (including the horses). Sadly, Jessica Springsteen missed the cut for this year’s Olympic Games, but hopefully the rest of the equestrian team will be inspired by her dad’s iconic hit “Born in the USA” …now doesn’t that make you feel patriotic!

Like Olympians, we at Ulrich strive for perfection and delivering results every day. We know that success is dependent on teamwork, and it would not be possible without the hard work of all our employees, constantly striving for the gold, and carrying the torch for you, our clients. We realize investing is not a game, set, match, but a life-long sport and we appreciate your trust and confidence in allowing us to coach you along the way!!

Regards,

John P. Ulrich, CFP®

President

Whitney E. Solcher, CFA®

Chief Investment Officer

Equity Markets

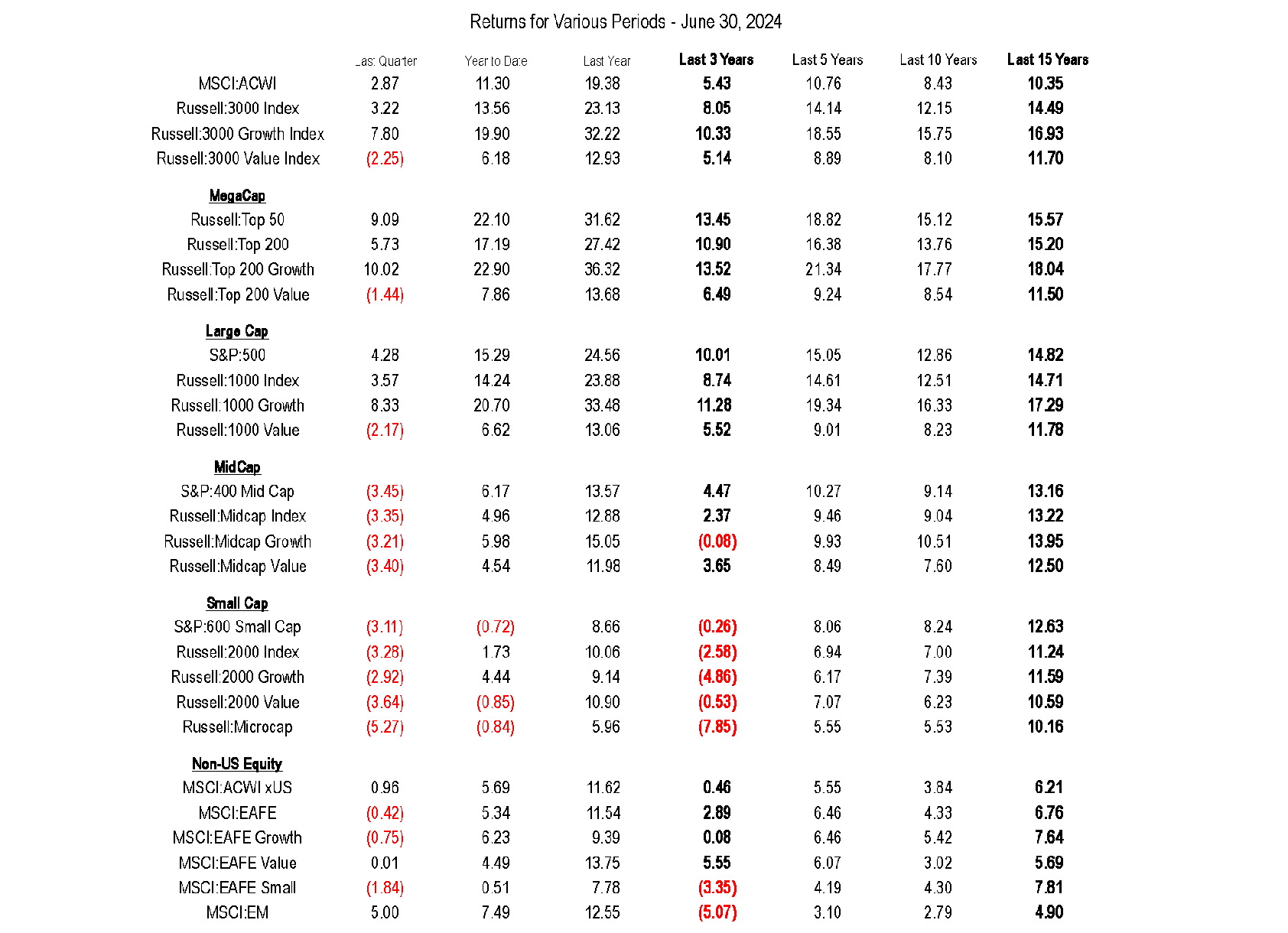

The S&P 500 Index hit 31 record highs over the first six months of 2024 and gained 15.3%. Second quarter results (+4.3%) were very mixed with sector performance ranging from -4.5% (Materials) to Technology (+13.8%) with 6 of the 11 S&P 500 sectors posting negative 2Q returns. Index returns were driven by a handful of stocks; the 10 largest stocks in the index returned 14% while the equal-weighted S&P 500 fell 2.6% for the quarter. Value (R1000V: -2.2%) sharply underperformed Growth (R1000G: +8.3%) and small cap (R2000: -3.3%) underperformed large (R1000: +3.6%). The Magnificent Seven comprised 33% of the S&P 500 as of quarter-end and, as a group, they climbed 33% in the first six months of the year, far exceeding the “S&P 500 ex-Mag Seven” gain of only 5%. However, there was much dispersion within this group as noted by the worst YTD return (Tesla: -20%) vs. the highest (NVIDIA: +150%).

The MSCI ACWI return (+2.9%) was attributable to only five stocks (NVIDIA, Apple, Alphabet, Microsoft, and Taiwan Semiconductor), four of which are U.S. companies. The remaining 9,000-plus stocks were down 0.1%. The MSCI ACWI ex-USA eked out only a modest gain of +1.0%. France (-7.5%) was a notable underperformer given concerns over the advancement of the far right and implications for spending and increases in an already high deficit. Japan (-4.3%) was a notable underperformer but in local terms the country was up 1.8%. The yen fell about 6% in 2Q to its weakest level since 1986. The currency is down 12.4% YTD.

Emerging markets (MSCI EM: +5.0%; Local: +6.2%) also saw mixed results. Latin America (-12.2%) fared the worst driven by poor returns in Brazil (-12.2%) and Mexico (-16.1%). Meanwhile, Emerging Asia (+7.4%) benefited from strong performance in China (+7.1%) and Taiwan (+15.1%). India (+10.2%) was also up sharply for the quarter in spite of a short-lived sell-off after the election.

Fixed Income Markets

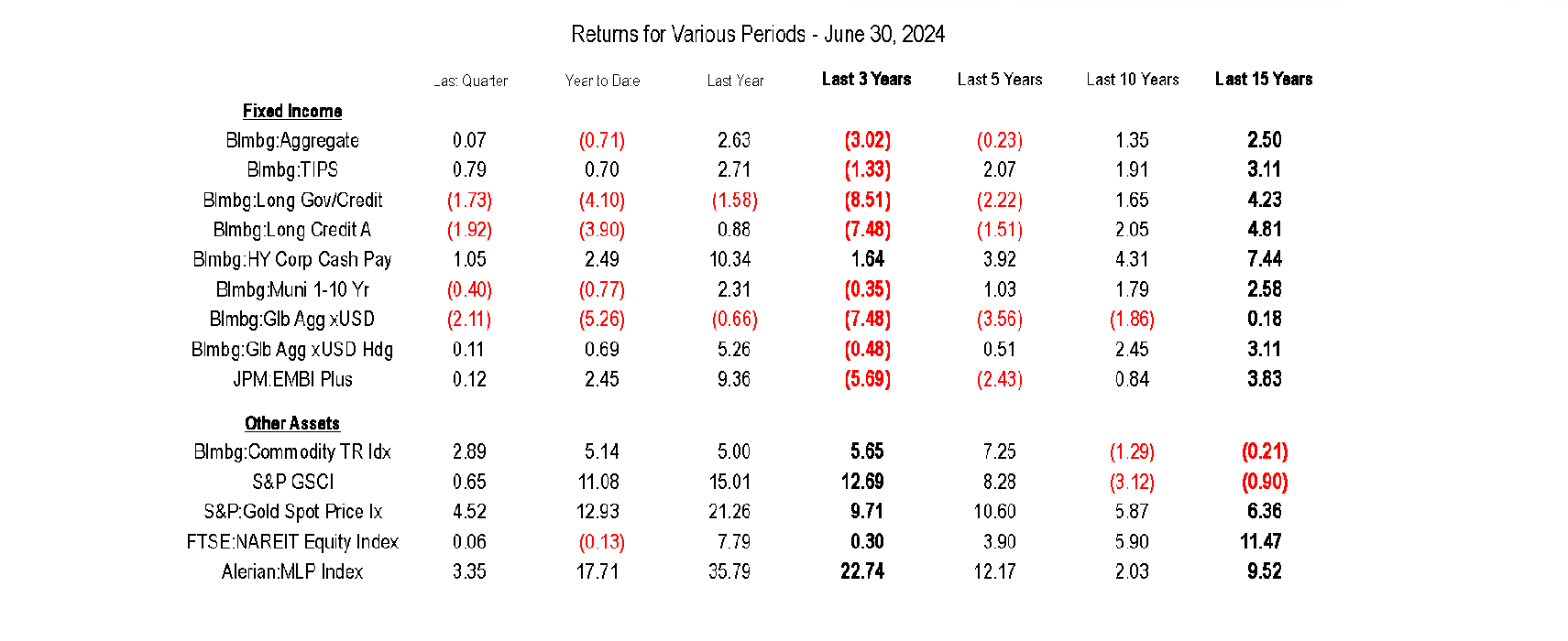

The Bloomberg US Aggregate Bond Index (+0.1%) was flat in 2Q, bringing its YTD return to -0.7%. The yield on the 10-year U.S. Treasury climbed from 4.20% to 4.36% over the quarter. Mortgages were the only sector to underperform U.S. Treasuries on a duration-adjusted basis. High yield (Bloomberg High Yield: +1.1%) and bank loans (Morningstar Leveraged Loan: +1.9%) were top performers for the broader market. Valuations, as measured by spreads, remained rich from a historical perspective across the credit spectrum as absolute yields attracted buyers less interested in relative value. Supply was robust but met with strong demand.

Global bond returns were also flat (Bloomberg Global Aggregate USD Hedged: +0.1%) while dollar strength eroded returns in unhedged terms (Bloomberg Global Aggregate Unhedged: -1.1%). Emerging market performance was similarly uninspiring with the hard currency JPM EMBI Global Diversified Index up 0.3% and the local currency JPM GBI EM Global Diversified Index down 1.6%. Brazil (-10.7%) and Mexico (-9.6%) were notable underperformers in the latter given currency weakness.

Municipal bond returns (Bloomberg Municipal: 0.0%) were also muted in 2Q. Yields rose most sharply in five- and seven-year maturities (44 bps), causing intermediate indices to underperform the broad market. The Bloomberg Muni 1–10 Year Index fell 0.4% for the quarter. Lower-rated bonds outperformed (AAA: -0.3%; BBB: +0.7%). Issuance in 2024 is more than 40% ahead of last year and the strongest in at least a decade but has been met with strong demand.

The views expressed represent the opinion of Ulrich Investment Consultants. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from sources that have not been independently verified for accuracy or completeness. While Ulrich Investment Consultants believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Ulrich Investment Consultants’ view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.